All Categories

Featured

Table of Contents

Below is a theoretical comparison of historical efficiency of 401(K)/ S&P 500 and IUL. Let's presume Mr. SP and Mr. IUL both had $100,000 to conserved at the end of 1997. Mr. SP invested his 401(K) money in S&P 500 index funds, while Mr. IUL's cash was the money value in his IUL plan.

IUL's policy is 0 and the cap is 12%. Because his cash was saved in a life insurance policy, he doesn't need to pay tax!

Horace Iule Cross

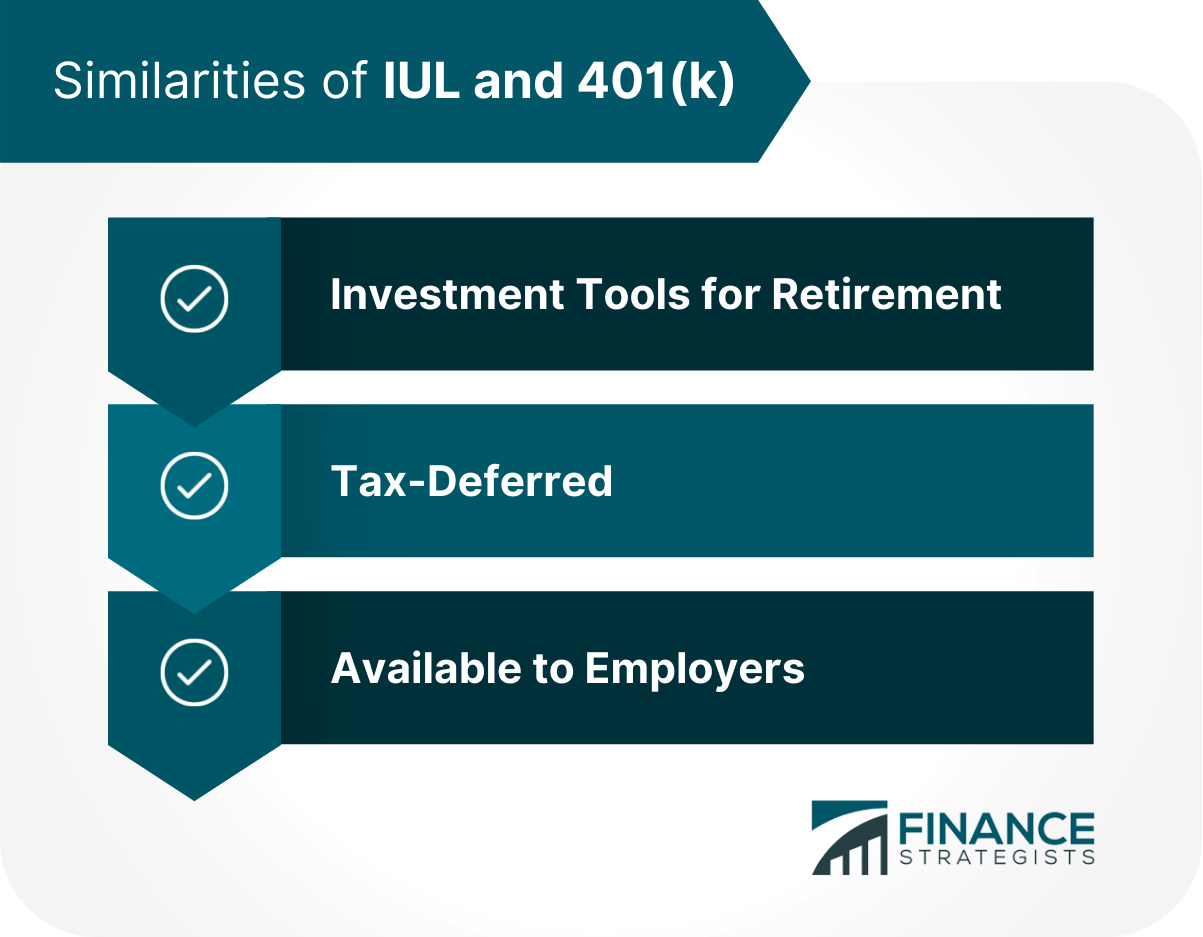

The countless selections can be mind boggling while investigating your retirement spending alternatives. There are certain choices that must not be either/or. Life insurance policy pays a survivor benefit to your beneficiaries if you ought to pass away while the policy holds. If your family members would deal with economic difficulty in the event of your fatality, life insurance policy uses comfort.

It's not one of the most profitable life insurance coverage financial investment plans, yet it is among one of the most secure. A type of long-term life insurance policy, global life insurance coverage enables you to pick just how much of your costs goes towards your death advantage and just how much enters into the policy to build up money worth.

In addition, IULs enable insurance holders to secure car loans versus their plan's cash money worth without being strained as income, though unsettled balances may be subject to taxes and fines. The main benefit of an IUL plan is its potential for tax-deferred growth. This implies that any type of incomes within the plan are not strained until they are taken out.

On the other hand, an IUL plan might not be one of the most appropriate financial savings prepare for some individuals, and a standard 401(k) can confirm to be much more useful. Indexed Universal Life Insurance Policy (IUL) policies provide tax-deferred growth capacity, defense from market downturns, and survivor benefit for recipients. They permit insurance policy holders to earn passion based on the efficiency of a stock market index while safeguarding against losses.

Iul Vs Ira: Key Differences For Retirement Savings

A 401(k) plan is a popular retired life savings choice that permits individuals to spend money pre-tax into various financial investment devices such as shared funds or ETFs. Companies may additionally supply matching contributions, additionally improving your retirement savings possibility. There are two major sorts of 401(k)s: standard and Roth. With a traditional 401(k), you can lower your gross income for the year by adding pre-tax dollars from your paycheck, while likewise gaining from tax-deferred growth and company matching contributions.

Lots of employers also give coordinating contributions, effectively offering you cost-free cash in the direction of your retirement. Roth 401(k)s feature likewise to their conventional equivalents yet with one key difference: tax obligations on payments are paid ahead of time as opposed to upon withdrawal during retirement years (How Does a Roth IRA Compare to IUL for Retirement Savings?). This means that if you anticipate to be in a greater tax bracket during retired life, adding to a Roth account might minimize taxes gradually contrasted with spending exclusively through standard accounts (source)

With reduced monitoring charges generally contrasted to IULs, these sorts of accounts allow financiers to save money over the long-term while still gaining from tax-deferred growth potential. Additionally, numerous popular affordable index funds are available within these account types. Taking distributions before getting to age 59 from either an IUL plan's cash value through fundings or withdrawals from a conventional 401(k) plan can lead to negative tax implications otherwise taken care of meticulously: While borrowing against your policy's money worth is normally thought about tax-free up to the amount paid in costs, any kind of overdue lending equilibrium at the time of fatality or policy abandonment may be subject to revenue taxes and penalties.

Iul Vs Traditional 401k

A 401(k) supplies pre-tax investments, employer matching payments, and possibly even more financial investment selections. iul agent near me. Seek advice from a monetary planner to figure out the very best choice for your situation. The downsides of an IUL consist of higher management expenses contrasted to conventional retired life accounts, restrictions in financial investment choices because of plan constraints, and prospective caps on returns during strong market performances.

While IUL insurance might verify beneficial to some, it's important to recognize how it functions before acquiring a plan. Indexed global life (IUL) insurance plans supply higher upside prospective, versatility, and tax-free gains.

firms by market capitalization. As the index moves up or down, so does the rate of return on the cash money worth component of your policy. The insurer that releases the policy may provide a minimum guaranteed rate of return. There might also be a ceiling or rate cap on returns.

Economic experts commonly advise having life insurance coverage that's equivalent to 10 to 15 times your annual earnings. There are numerous downsides related to IUL insurance coverage that doubters fast to aim out. Someone who develops the policy over a time when the market is performing improperly could end up with high costs payments that don't contribute at all to the cash value.

In addition to that, remember the complying with other factors to consider: Insurer can set engagement prices for just how much of the index return you get each year. For instance, allow's say the plan has a 70% involvement rate (IUL vs 401(k) Comparison: Best Retirement and Investment Options). If the index expands by 10%, your cash worth return would be only 7% (10% x 70%)

In enhancement, returns on equity indexes are frequently covered at an optimum quantity. A plan might claim your maximum return is 10% per year, regardless of just how well the index carries out. These limitations can limit the real rate of return that's attributed toward your account yearly, regardless of just how well the plan's underlying index does.

美国 保单 Iul 费用 说明

IUL plans, on the other hand, offer returns based on an index and have variable costs over time.

There are lots of other kinds of life insurance policy plans, described listed below. offers a fixed benefit if the policyholder passes away within a collection amount of time, usually between 10 and three decades. This is among one of the most affordable sorts of life insurance policy, in addition to the easiest, though there's no cash worth accumulation.

Iul Vs Ira: Choosing The Right Option For Your Financial Goals

The plan obtains worth according to a taken care of schedule, and there are less fees than an IUL plan. A variable policy's cash value may depend on the efficiency of specific stocks or various other protections, and your premium can additionally change.

IUL insurance is an essential tool for the infinite banking strategy. insurance brokers for IUL financial planning. Infinite banking with Indexed Universal Life lets you become your own banker

Using your Indexed Universal Life's cash value as collateral, you can invest in opportunities while your money continues to grow tax-free. Insurance brokers specializing in IUL help you customize IUL policies for financial freedom.

With features like cash value growth and tax-free loans, IUL supports flexible financial strategies. Learn how IUL can transform your finances with a free consultation from a licensed broker.

{kind=link}

Latest Posts

Indexed Universal Life Insurance Complaints

Universal Life Guaranteed Death Benefit

Eiul Policy